October 6, 2021

by DH Kim, CEO Finhaven

Background: Capital market volatility is revisiting us along with Fed’s tapering, and inflation & fear of debt (Evergrande and US debt ceiling).

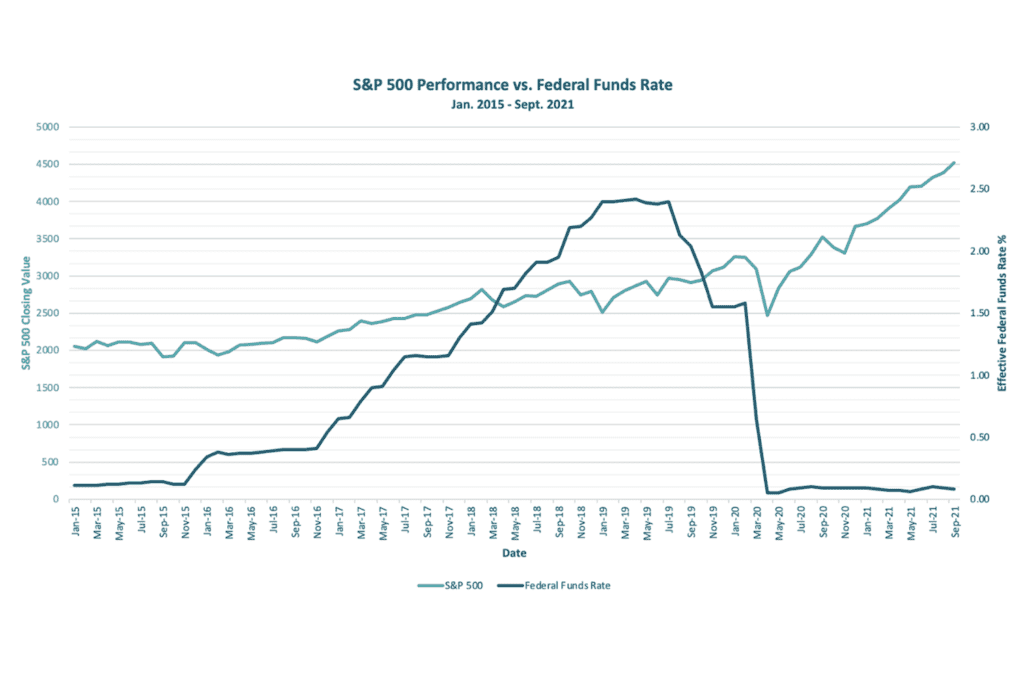

Long-term view: Tapering by the Fed will end in the middle of 2022, and the US central bankers will consider hiking the Fed funds rate. With the inflationary trend lasting longer than expected, the urge to raise the rate is likely to grow in the coming months. The Fed started raising the Fed funds rate in late 2015. The average yield in 2015 was 0.13%, and reached 2.16% in 2019. S&P 500 performed at 13.5% per annum (dividend reinvested) from November of 2015 to February 2020. The return was not bad at all. (See chart above.) Because the Fed funds rate will rise with the economic growth, the rate increase should not be a fear factor.

Difference to note: Although global GDP had substantially contracted by 5.93% in 2020, and as the global economy is not fully recovered in 2021, we are still seeing inflation due to global supply chain disruption. This is a big difference from the circumstances of 2014 and 2015. The key variable will be how quickly the world returns to normal with Covid-19. This variable will determine whether the current inflationary trend will be temporary. Temporary inflation with the gradual yield increase will be ideal for capital markets.

US debt ceiling: It is politics, a Republican’s bargaining chip. Republicans will get what they want and lift the US debt ceiling.

Evergrande: China is a large, relatively closed, controlled economy. Therefore, the catastrophe of Evergrande will unfold in an orderly fashion, unlike that of Lehman Brothers. Remember, the Chinese government owns the land in China. In addition, such major lenders as Agricultural Bank of China, China Minsheng Banking Corp, and China Citic Banking Corp are strongly influenced by the Chinese government. The immediate implication of Evergrade’s trouble will be limited, but it is noteworthy that the change in the Chinese real estate market following this incident may negatively affect the growth trend of China.

A good leading indicator: South Korea’s exports is a good leading indicator for the global economy as Korea’s economy is driven by exports spanning various industries. Since April 2021, the data shows very strong growth, over 30% YoY in many weeks ranging from semiconductor and automobile to steel.

Please visit finhaven.com and finhaven.ca to invest in alternative assets including private securities and crypto-assets.